As a result of their rapid growth and of the dynamics of their development, the BRIC countries and emerging markets are now highlighting their increasing weight in the global economy by taking on an ever-greater role as international investors. But if we look behind these common characteristics, the dynamics and modes of their investments and the strategies of their multinational corporations stand in sharp contrast to one another.

BRICs and Emerging Markets

The New International Investors

|

The economies of emerging markets experienced exceptional growth in the 2000s, to the extent that some economists believed they would be left untouched by the financial crisis and global recession. At the forefront of these emerging markets stand Brazil, Russia, India and China (the BRICs). Despite the fact that it is rapidly growing, the foreign direct investment (FDI) of these countries has garnered less attention and comments than their economic growth, while the crisis caused a fall in total FDI throughout the world. This illustrates the resilience of these emerging markets in the face of the crisis. The fastest-growing multinational corporations (MNCs) today are no longer those that are based in developed countries, particularly since the start of the financial crisis that began in 2008. Rather, it is those based in emerging markets, and in particular the MNCs originating from the four BRICs. Should this come as a surprise? No.

Indeed, a famous economic theory of FDI, developed by John Dunning [1], explains that it varies depending on the level of economic development of each country. During a first stage, when a country is under-developed, it receives little direct investment from abroad (inward FDI), and does not itself invest abroad (no outward FDI). During a second stage, once it has become a developing country, this country becomes attractive to inward FDI on its territory, but still carries out little outward FDI abroad; it is a net importer of FDI (its inward FDI imports are greater than its outward FDI exports). During a third phase, thanks to its new technological abilities and its low unit labour costs, a country emerges as an increasingly significant investor abroad, even if it still receives more inward FDI than it issues outward FDI (it remains a net importer of FDI). This is what we are currently observing in the case of emerging markets and BRICs: they are reaching this third stage of economic development, including from the perspective of their FDI. This aspect of Dunning’s theory has already been verified using econometric tests [2]. During a fourth stage, a developed country tends to invest far more abroad than it receives investments from foreign firms (it then becomes a net exporter of FDI). A final stage is then reached, that of the post-industrial society, in which a country, which must then rank among the most developed in the world, more or less balances its outward and inward FDI, as is the case with the United States for example.

The expansion of MNCs that originate in emerging markets is not just an index of the relative resistance of these countries during the crisis, following a phase of strong economic growth during the 2000 decade – it is also a more qualitative phenomenon that marks their moving into a higher state of development, and towards a certain convergence with developed countries. We can therefore expect to observe certain similarities between the MNCs of emerging markets and their strategies for foreign investment, especially if we use a sample reduced to the four BRICs.

Rapid Growth and Similarity of Multinational Corporations Originating from the BRICs

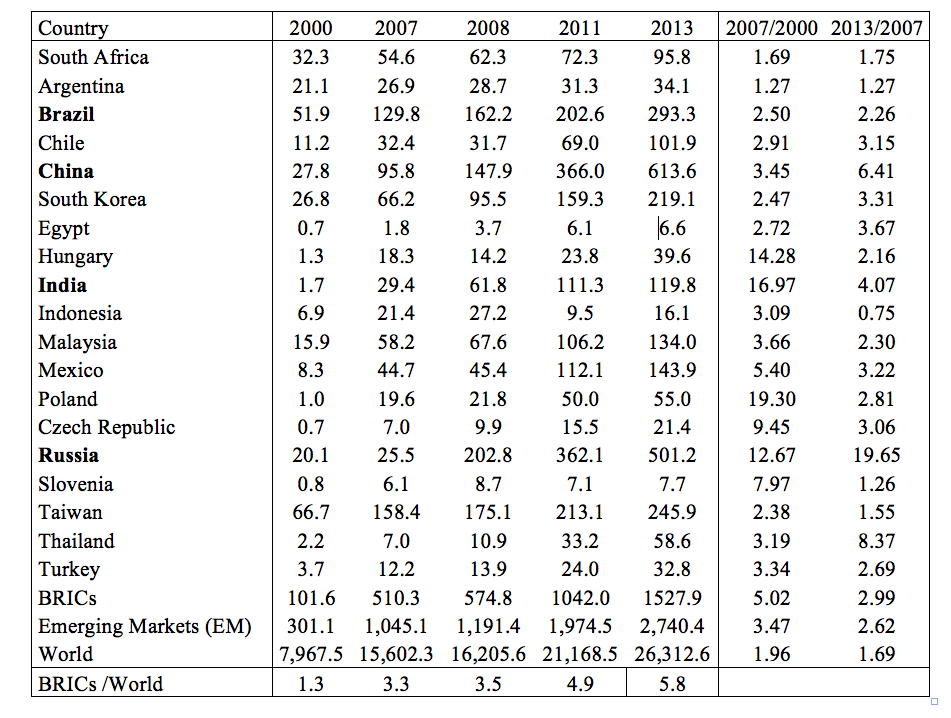

We can first observe, in Table 1, the very rapid growth of the outward FDI stock of 19 emerging markets [3]: its value was multiplied by 3.5 before the crisis, and by 2.6 during the crisis, while that of the outward FDI of all MNCs in the world was only multiplied by 2 and 1.7 respectively. Within emerging markets, the multiplication is substantially stronger in the case of the outward FDI of the four BRICs that we are focussing on here. In 2013, the outward FDI of emerging markets made up over 10% of the global total, and that of the BRICs almost 6%.

Table 1 – Outward Foreign Direct Investment of Emerging Markets

(Stock in Billion Dollars)

Source: Calculated based on the World Investment Report (UNCTAD).

Grouping the BRICs together is justified by similarities between their MNCs, though these should not obscure certain specific aspects of their strategies, often connected to their countries of origin and to the relationships that they have with the state in said countries.

Indian corporations began investing abroad as early as 1955, with Birla in Ethiopia. Brazilian MNCs such as Petrobras or Copersucar emerged in the 1970s, while Chinese MNCs opened their first foreign subsidiaries from 1979. The first instances of Russian outward FDI started in 1994 and did not intensify until 1998. Chinese and Russian outward FDI, which started last, rapidly caught up with the others: in 2008, the total amount of Russian outward FDI exceeded that of the other BRICs, and in 2011 it was in turn overtaken by the total amount of Chinese outward FDI. One major difference is that Indian and Chinese MNCs based their expansion abroad on the experience known as linkage, leverage and learning in contact with MNCs from developed countries that had previously invested in their countries, as well as on technology transfers from these foreign corporations. This model did not work so well in Brazil, and practically not at all in the case of Russian corporations, since Russia remained relatively closed to inward FDI compared to the other BRICs.

The golden age of growth of emerging MNCs took place in the years between 2000 and 2007. Since 2008, the financial crisis has, in one year or another, restricted Russian, Brazilian or Indian outward FDI, though never Chinese outward FDI, which does not seem to have been affected by the crisis. From 2007 to 2013, among the BRICs, China saw the most stable and substantial growth in its outward FDI, Russia saw the most irregular and rapid growth, and Brazil the slowest growth on average.

Brazilian MNCs include both major competitive corporations such as Embraer, Vale, Petrobras (all ‘global players’) and SMEs. Indian MNCs are conglomerates (Tata, Birla) or family businesses (Bharat Forge, Mahindra & Mahindra) that have developed a specific technological expertise. Russian MNCs, which were initially lacking in transparency (Gazprom, Rusal, Rosneft), are moving closer to a real global strategy, which is the preserve of Chinese MNCs, despite the fact that most of them are state-owned corporations. All of them develop through the widespread use of takeovers and mergers with existing foreign corporations, with the aim of appropriating their assets, often technological assets: thus, Mittal bought Arcelor, Geely bought Volvo, Petrobras bought Pasadena Refining (US), and Rusal bought SUAL Glencore (Switzerland).

The main motivation of the vast majority of MNCs from the BRICs consists in investing abroad in order to be close to their markets (a strategy known as market seeking), with investment often replacing prior exports. The second motivation for outward FDI (which is then known as resource seeking) is to appropriate or control natural resources (oil, gas, ore) located abroad in order to guarantee supply to their home country or to maintain a monopoly in certain sectors of raw materials (Russian and Brazilian MNCs). Chinese and Russian MNCs are more attracted to technological asset takeovers (asset seeking) from their foreign rivals through takeovers and trans-border mergers. Indian MNCs less often resort to this strategy, especially in the industries where they are very close to the global technological level (pharmaceuticals, IT). Only Chinese and Indian MNCs have already significantly delocalised certain activities to less developed countries in Asia and Africa in order to gain advantage of the lower unit labour costs [4] compared to their home countries (a strategy known as efficiency seeking), a trend which is growing stronger with the wage rises that have taken place in China in recent years.

The geographic orientation of outward FDI from the various BRICs is very similar. Their first destination is free zones and tax havens: 43% of Brazilian outward FDI, 58% of Russian outward FDI, 75% of Chinese outward FDI, less in the case of India. The aim is to remove the relevant capital from the investment regulations and taxation rates of their country of origin. Most often, tax havens act as hubs, with the capital that has been invested there then being reinvested into the third-party country being targeted by this or that BRIC-based MNC. One of these FDI circuits is very particular, namely the practice known as round tripping: for example, the outward FDI from a Russian corporation in Cyprus is then redirected towards – has as its ultimate goal – the Russian economy itself, or that of a Chinese corporation in Hong Kong is ultimately aimed at continental China [5].

The second most important geographic destination is developed countries. The third is constituted by neighbouring countries, be they bordering ones, or countries from the same region or continent. Thus, Russian MNCs are attracted to close foreign countries (i.e. the countries of the CIS), which still share the same business culture, and do business in Russian; Brazilian MNCs invest in Latin America, but also in Portuguese-speaking countries (Portugal, Angola, Mozambique) for similar reasons; Indian MNCs favour countries with a strong Indian diaspora, and Chinese MNCs those with a large Chinese diaspora. BRIC-based MNCs avoid investing in the least-developed countries in the world, although Chinese MNCs have recently increased their penetration in Africa in the name of the Chinese state’s Go Global strategy (zou chu qu).

The sectorial distribution of BRIC-based MNCs, at the start of their expansion, was concentrated in the primary sector and in industry. It is now more and more similar to that of Western and Japanese MNCs, with a substantial part of FDI being invested into services, banking and finance: 66% of Chinese outward FDI, 62% of Indian outward FDI, and 59% of Brazilian outward FDI. Only Russian outward FDI remains mainly connected to raw materials (oil, gas) and heavy industry (metallurgy, chemical industry), sectors that were inherited from the old Soviet model of development.

Highly Differentiated Stat Support from One BRIC to the Next

None of the four BRICs can claim that the expansion of their corporations through foreign investment was carried out completely independently from the state, or without any interference from it. But if we look beyond this strong similarity, there are fare more than subtle differences between, at the two extremes, the significant state strategy in China and the absence of any specific economic policy related to outward FDI in Brazil.

In China, ever since the adoption of the Go Global strategy in 1999, all the hierarchic levels of the central administration [6] have been mobilised to authorise, stimulate and support, but also control outward FDI and direct it towards this or that sector. Since 2003, every Chinese province has had the same prerogatives for outward FDI beneath 3 million dollars, and this decentralisation was generalised in 2009. When the 12th five-year plan was adopted in 2010, a strategy known as Accelerating Go-Out was launched, to promote outward FDI through easier access to payments in renminbi from 2011. Chinese outward FDI nevertheless remains very concentrated in the hands of the major state-owned corporations: 160 of these that are directly managed by the central state (the SASAC: State-owned Assets Supervision and Administration Commission) together hold 84% of total Chinese outward FDI. Their managers are appointed by the government and the Communist Party. Chinese MNCs enjoy a monopoly over the Chinese market, and engage in monopolistic practices abroad as well, which sometimes provokes hostile reactions in the countries hosting their subsidiaries. Because they benefit from privileged lines of credit and loans at low interest rates from Chinese state-owned banks, they have low capital costs, which constitutes a major competitive advantage compared to Western MNCs, which are subject to strong financial constraints. The old slogan “what’s good for General Motors is good for America” can be transposed to this situation: what’s good for Chinese MNCs is good for China’s state capitalism.

Although Yeltsin’s policies did not promote Russian outward FDI, privatisations created powerful, monopolistic corporations; they then played a role as the soft power (as opposed to military power) of Russia abroad, in particular in neighbouring countries (the CIS) and in Central and Eastern Europe. Under Putin’s presidency, the Russian state has moved towards promoting outward FDI at the service of its strategic goals, by relying on the expansion abroad of its ‘national champions’, the largest MNCs in the main Russian industries. This strategy was supported by a partial renationalisation of Russian industry during the 2000s, and an increasingly less clear division between government and business, with the election of Dmitry Medvedev, the former CEO of Gazprom, as President of the Russian Federation, or the appointment of Igor Sechin, the former CEO of Rosneft, as Deputy Prime Minister. Since 2007, Putin has been encouraging Russian corporations to export and invest abroad, and Medvedev has been calling on them to copy China. Nevertheless, Russia has still not precisely defined a policy to support the expansion of Russian MNCs, as China has done for its MNCs. The fossil fuel sector in particular is used as a tool at the service of Russia’s international policy, through the control of oil and gas pipelines and therefore of the exports that are transported through them. Russian MNCs are not independent from the state, especially not in this sector, nor of its expansionist ambitions in the CIS, in Asia and in Africa.

Indian outward FDI was restricted and controlled by an interventionist and planning state until 1991, and then benefited from the economic liberalisation that took place at this time. From 1992, outward FDI below a certain amount (100 million dollars in 2002) received automatic state approval; since 2004, no outward FDI requires state approval and Indian MNCs are entitled to invest or buy assets abroad even in sectors that are unrelated to their activity in India. Outward FDI only remains under the supervision of an inter-ministerial group in the banking and real estate sectors. Since 2005, Indian MNCs have had free access to international capital markets, and since 2007 they can finance their foreign subsidiaries through loans received from Indian banks. Since 2011, the state has been supporting public sector corporations in their foreign expansion through takeovers in the sector of raw materials. In the other sectors, outward FDI is mainly private and is not coordinated by the state as it is in China and Russia.

In Brazil, the state has no specific policy as regards outward FDI, even if since 2002 it has been possible for such investment to benefit from a dedicated line of credit. Brazilian MNCs must first rely on self-financing and funds obtained from abroad. The privatisations carried out in the 1990s encouraged the expansion of major formerly public MNCs such as Petrobras, Vale or Embraer, in which the state is still a (minor) shareholder. Finally, in the name of a policy of competitiveness, the Brazilian Development Bank offers incentives for mergers of Brazilian corporations, with each other or with foreign corporations. However, there are no fiscal incentives, nor any other state stimulant encouraging Brazilian outward FDI.

The dynamism of emerging markets means it makes sense to create a special category of countries undergoing rapid development, in particular in the case of the BRICs, which are involved in institutional rapprochements (BRIC summits, creation of an international bank as an alternative to the World Bank). Nevertheless, we observe that this group is heterogeneous, in this area as in others, as soon as we look into the details of their outward FDI and MNCs.

Conclusion

Ultimately, if we look beyond the similarities due to the fact that they are based in emerging markets, the BRICs’ MNCs and outward FDI also present specificities. The group of BRICs – and more widely of emerging markets – is not homogenous in terms of the economies that make it up; nor is it so in terms of their outward FDI. The divide between on the one hand Russian and Chinese MNCs, which arose out of post-Communist transitions, and on the other Brazilian and Indian MNCs, which arose out of market economies, does not explain everything. Thus, just like Russian and Chinese MNCs, Indian MNCs are on the lookout for technological assets abroad, while Brazilian MNCs are much less so. Brazilian and Russian MNCs do not invest much into the other BRICs, while Chinese are Indian corporations are very present in this space. The geographic distribution of Chinese outward FDI is more diversified than that of the other BRICs, which is probably why it was more resilient during the crisis.

The recent fall in oil and raw material prices has accentuated the differences between emerging countries even more, including within the BRICs. As major exporters of these raw products, Brazil and above all Russia are suffering from external deficits caused by the fall in price of their main exports. Decreasing export revenue and trade deficits translate into budget deficits for the state. Simultaneously, the fall in oil and raw material prices increases competition on these global markets and reduces Brazil and Russia’s external outlets (a phenomenon that has been worsened by European sanctions and the embargo in the latter case). These developments are sharpening the recession hitting the Brazilian economy and the fall in economic growth in Russia. Were they to last, they could ultimately have a negative impact on the outward FDI of these two countries, something that has already been observed in 2015 in Russia.

In contrast, India and China are seeing the price of a substantial fraction of their imports decrease, that of raw products: there is no trade deficit, and a less sharp slowdown of growth in India than in Brazil and Russia. As for the recession connected to the global crisis, it is indeed affecting China, but it has made the growth rate of GDP fall to 6 or 7% per year. This is still a very enviable rate for most countries in the world, and it should support the expansion of outward FDI from China and of Chinese MNCs.

by , 14 April 2016

Share this article

Find us here :

To quote this article :

Wladimir Andreff, « BRICs and Emerging Markets. The New International Investors », Books and Ideas , 14 April 2016. ISSN : 2105-3030. URL : https://laviedesidees.fr/BRICs-and-Emerging-Markets

Nota Bene:

If you want to discuss this essay further, you can send a proposal to the editorial team (redaction at laviedesidees.fr). We will get back to you as soon as possible.

You might also like

Footnotes

[1] J.H. Dunning, Explaining the International Direct Investment Position of Countries: Towards a Dynamic or Development Approach, Weltwirtschaftliches Archiv, 119, 1981, 30-64.

[2] In particular as far as his section on outward FDI is concerned: W. Andreff, The Newly Emerging TNCs from Economies in Transition: A Comparison with Third World Outward FDI, Transnational Corporations, 12 (2), 2003, 73-118.

[3] These are the countries that appear in all the lists of emerging markets drawn up respectively by the IMF, Boston Consulting Group, Standard & Poor’s and BNP Paribas.

[4] Wage divided by labour productivity.

[5] Round tripping is estimated to make up 50% of Chinese FDI in Hong Kong.

[6] For a description of the bodies that have an influence on Chinese outward FDI, please see: W. Andreff, “Maturing strategies of Russian multinational companies: Comparison with Chinese multinationals”, in: D. Dyker, ed., Foreign Investment, The World Scientific Reference on Globalisation in Eurasia and the Pacific Rim, Imperial College Press/World Scientific, London 2016.

Our partners

Sections

Keep in touch

© laviedesidees.fr - Any replication forbidden without the explicit consent of the editors. - Mentions légales - webdesign : Abel Poucet